Lesson 4

Business metrics

October 23, 2024

Structure

Definitions

Cost classification

Fixed and variable costs

Variables to measure company’s result

1. Definitions

Revenues

Revenue, often referred to as sales or the top line, is the money received from normal business operations

Accounting includes sales made on credit as revenue for goods or services delivered to the customer. Under certain rules, revenue is recognized even if payment has not yet been received.

Revenue = Quantity Sold x Unit Price

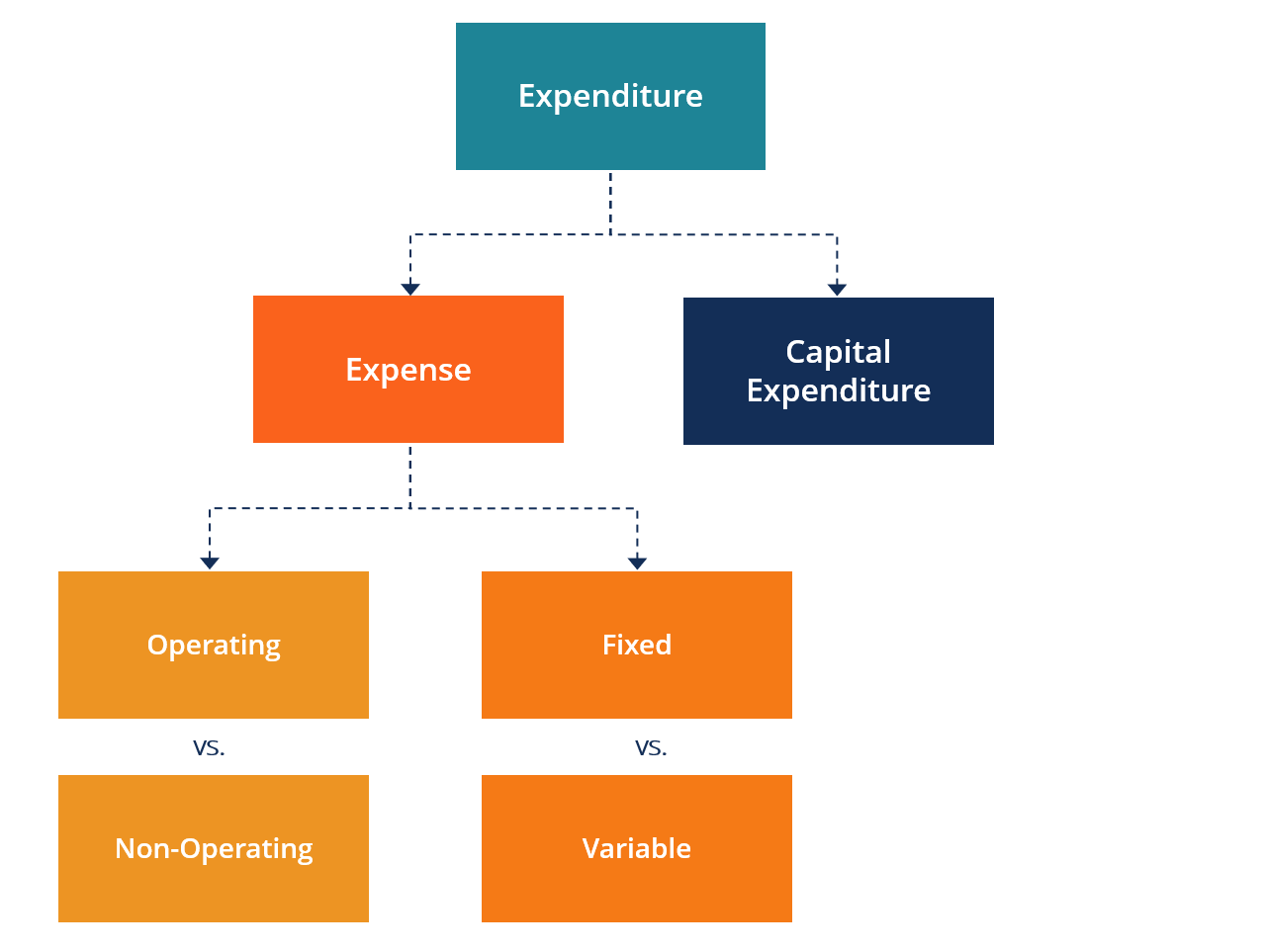

Expenditure

- Payment with either cash or credit to purchase goods or services

Expenses

- Cost of operations that a company incurs to generate revenue

Expenses are recognized when they are incurred, not necessarily when they are paid for

Expenses are reported on the income statement

Cost

Expenditure required to produce or sell a product or get an asset ready for normal use.

Amount paid to manufacture a product, purchase inventory, sell merchandise or get equipment ready to use in a business process

Cost and expense frequently intermingled

🎥 video on cost definition (just the first minute)

Profits

Difference between the revenue received from the sale of an output and the cost of all inputs

Economic profit vs Accounting profit

Accounting profit: revenue - expenses. Total earning of a company

Economic profit: revenues - expenses - opportunity costs

Accounting profit = net income

Structure

Definitions

Cost classification

Fixed and variable costs

Variables to measure company’s result

2. Cost classification by nature

C1. Material costs

C2. External services costs

C3. Depreciation costs

C4. Labour costs

C5. Opportunity costs

C1. Material costs

Cost of materials used to manufacture a product or provide a service

Prices paid for raw material components and purchased finished goods, including any packaging necessary for the shipment of products, which are purchased from outside vendors as well as any freight and duty where applicable

Raw materials, spare parts, sub-assemblies, packaging materials, commodities, etc

Boeing aircrafts raw materials

C1. Material costs II

Sub-assemblies: Aircraft construction begins with the assembling of detail parts into aircraft sub-assemblies. Positioned adjacent to one another these aircraft sub-assemblies make the final assembly of the aircraft. To prevent these aircraft sub-assemblies from a wrong location and position, tooling fixtures are used throughout the assembly process. Tooling fixtures locate the detail parts of aircraft sub-assemblies, and then these are attached to mating aircraft structure (definition from Lockheed Martin Corporation link)

Aerospace supplier chain tiers:

Tier 1: major components or systems who receive parts

or subassemblies from the Tier 2 supply chain. Engines, control systems, landing gear, braking systems, flight deck, avionics, aerostructures, electronic warfare systems and interior cabin productsTier 2: manufacture of parts or subsystem assemblies

used by Tier 1 companies. Airfoils and tires, missile nose cones and airframe structures, transmissions and flight controlsTier 3: component manufacturers that ship their products directly to Tier2. Hydraulic fittings and hose, instrumentation fittings and tubing, high strength fasteners and pins

- Reading on aerospace supplier chain tiers

C1. Material costs III

Products have extremely long life cycles of 30 years or more, during which they need to provide legacy-parts support.

But the internal components for those systems, including semiconductors, electronic boards, and mechanical parts, have much shorter life cycles, in some cases less than five years.

Because of this disparity—the “two speed” challenge—components can become harder to source over time and even grow obsolete as suppliers struggle to source the raw materials or stop manufacturing them altogether

As a result, manufacturers must design replacements for those obsolete components and face nonrecurring engineering costs as a result.

C1. Material costs IV

Shortly after becoming CEO of Ford Motor Co., the former head of Boeing Commercial Airplanes,

Alan Mulally, was asked if he was ready for the complexity of the automotive industry.

He replied;

“An automobile has about 10,000 moving parts, right? An airplane has 2 million, and it has to stay up in the air,”

C2. External services

Services provided by external providers to the contracting company such as:

Transport and logistics

Maintenance

Leasing

Insurance

Financial services: loans

Accounting

Backoffice

Legal

Tech support

Software development

and others

Outsourcing. Is it always good?

C3. Depreciations

Decline in value of assets

Allocation of the cost of tangible assets to periods in which the assets are used

Businesses need to account for the consumption of fixed assets over time in a way that reflects their reducing value, this is termed as ‘depreciation’

Working out depreciation presents problems and requires acknowledge about :

Taxation policy

Maturity (lifespan)

Residual value (scrap value, salvage value)

Amount to be depreciated

Depreciation method

C3. Depreciation II

Example:

Extracted from How to depreciate property. Publication 946. Department of Treasury:

You can depreciate most types of tangible property (except land), such as buildings, machinery, vehicles, furniture, and equipment. You can also depreciate certain intangible property, such as patents, copyrights, and computer software.

To be depreciable, the property must meet all the following requirements.

It must be property of your own

It must be used in your business or income-producing activity

It must have a determinable useful life

It must be expected to last more than one year

C3. Depreciation III

The fixed assets are valued at the price of acquisition (market price) or at the production cost: purchase cost + expenses (all kind of expenses until the asset is running)

All fixed assets, with the exception of land, suffer physical depreciation and obsolescence

The depreciation is an expense (cost) that is accounted in the Income Statement

Types of depreciation:

Physical depreciation

Functional depreciation

Obsolescence

The useful economic life of an asset is the total time, measured in years, that the asset is in conditions to produce goods and services. The period in which the asset is expected to be used by the entity in its business

C3. Depreciations IV

The useful life of an asset will be the lower between:

Physical or mechanical: timespan without decreasing productivity. Most of the assets suffer from wear and tear: physical deterioration through usage

Technical life or obsolescence: physical conditions can be right but the asset can be replaced for technological reasons (new models ->higher productivity)

End of the product life cycle

Obsolescence in avionics: upgrade (retrofit) vs aftermarket (spare sets)

Straight-depreciation method

To estimate the annual depreciation expense (d), you need to know:

Useful life of the asset (t)

Cost of the fixed asset (V0)

Residual value (salvage or scrap value) of the asset (Vr)

Then you can estimate:

- Total depreciation and (book) value of the asset in the period n

Straight-depreciation method II

Being:

d: annual depreciation d=V0−Vrt

Vo: value of the asset at t=0

Vr: residual value

t: lifespan

Accumulated depreciation in the nth year: Da=V0−Vrt⋅n=(V0−Vr)⋅nt

Book value of the asset in n-year: Vn=V0−Da

Amount to depreciate: Vp=(V0−Vr)−Da

Depreciation tables

The Spanish official depreciation tables state (tax purposes):

The maximum annual rate, constantly applied, it estimates the minimum period for depreciating each asset according to tax regulations

And the maximum period for depreciating the asset completely

Depreciation tables II

Depreciation tables III

Depreciation in airlines

Aircraft are depreciated using the straight-line method

over their average estimated useful life of 20 years,

assuming no residual value for most of the aircraft of

the fleet. This useful life can, however, be extended to

25 years for some aircraft.

During the operating cycle, and when establishing fleet

replacement plans, the Group reviews whether the

amortizable base or the useful life should be adjusted

and, if necessary, determines whether a residual value

should be recognized.

Since 2013, new commercial aircraft and reserve

engines have been depreciated over a period of 20

years to a residual value of 5 per cent.

Assets acquired second-hand are depreciated over their

expected remaining useful life

Aircraft are depreciated using the straight-line method

over their average estimated useful life of 20 years,

assuming no residual value for most of the aircraft of

the fleet. This useful life can, however, be extended to

25 years for some aircraft.

Ryan Air depreciation policy

Extracted from Ryan Air Annual Report 2024

Ryan Air depreciation policy II

Extracted from Ryan Air Annual Report 2024

Rotable spare parts held by the Company are classified as property, plant and equipment if they are expected to be used over more than one period.

Ryan Air depreciation policy III

Intangibles Assets:

Extracted from Ryan Air Annual Report 2024

Typical depreciation rate information for different aircraft types

Factor affecting the depreciation rate in airlines

Effective depreciation rates for individual components are determined by the estimated useful life and residual value.

Determining an appropriate depreciation rate is dependent on a number of factors including:

• Intended life of the fleet type being operated by the airline

• Estimate of the economic life from the manufacturer

• Fleet deployment plans including timing of fleet replacements

• Changes in technology

• Repairs and maintenance policies

• Aircraft operating cycles (long-haul aircraft may have a different depreciation profile to high cycle short-haul aircraft)

• Prevailing market prices and the trend in price of second hand and replacement aircraft (which impact the estimate

of residual value)

• Aircraft-related fixed asset depreciation rates, for example, rotables and repairables may reflect the airline’s ability

to use common components across different aircraft types

• Treatment of idle assets

• Distinction between fleet types

Depreciation exercise 1

An airline company is buing a passanger aircraft, specifically a Boeing 737-800 for 82 million $

Build a depreciation table for the following cases:

Maximum period (Spanish law), no residual value

AirFrance-KLM: minimum period, 4% residual value

Exercise 2. Depreciation

AirChina is overhauling two engines for 6 million $ each. Assuming a 5-year useful life after the overhauling and a 7% residual value, work out the annual depreciation of both engines

C4. Labour expenses

The cost of labour is the sum of all wages paid to employees and the cost of employee benefits and payroll taxes paid by an employer

Salary

Social Security

Employee benefits: perks

C5. Opportunity costs

The value of the next-best alternative when a decision is made

Potential forgone profit from a missed opportunity

The value of what you lose when choosing between two or more options

What must be given up to obtain something that is desired

Structure

Definitions

Cost classification

Fixed and variable costs

Variables to measure company’s result

3. Fixed and variable costs

Variable costs

A variable cost is an expense that changes in proportion to production output or sales

When production or sales increase, variable costs increase

When production or sales decrease, variable costs decrease

Variable costs are a central part in determining a product’s contribution margin

Examples of variable costs include raw materials, labor, utilities, commission, or distribution costs

Fixed costs

A cost that does not change with an increase or decrease in the number of goods or services produced or sold

These costs are set over a specified period of time and do not change with production levels

They are usually established by contract agreements or schedules

Once established, fixed costs do not change over the life of an agreement or cost schedule

Depreciation is one common fixed cost

Structure

Definitions

Cost classification

Fixed and variable costss

Variables to measure company’s result

4. Variables to measure company’s results

EBITDA = Earnings before interest, taxes, depreciation and amortisation

EBIT = Earnings before interest and taxes

Both EBIT and EBITDA strip out the cost of debt financing and taxes

Both focus on the operation side

Companies with high fixed assets will have higher depreciation and so lower EBIT than companies with lower levels of fixed assets

Variables to measure company’s results II

Profits

Net income for a company or revenus minus expenses

Profit (loss) before income tax

Profit (loss) after income tax

Accounting profit shows the amount of money left over after deducting the explicit costs of running the business

Explicit costs include labour, inventory needed for production, and raw materials, together with transportation, production, and sales and marketing costs

Accounting profit differs from economic profit as it only represents the monetary expenses a firm pays and the monetary revenue it receives (remember opportunity cost)

Variables to measure company’s results III

Cash flows:

Revenue - C1 - C2 - C4 - Income tax = Operation cash flows

EBITDA (1-t) = Operation cash flows

Measure of the cash obtained, costs without payments are not considered (depreciations)